The Future of Petroleum Refining in California Is Not More Oil Drilling

California state officials are suddenly panicked over the oil industry’s claim that declining in-state petroleum refining capacity is going to cause a spike in gasoline pump prices to over eight dollars a gallon. There is little empirical evidence to support this overheated prediction. To the contrary, there are good evidence-based reasons to believe that, absent industry price-gouging, pump prices will not be significantly affected as California continues to transition away from fossil transportation fuels. Let’s examine the reality behind the rhetoric.

There is no question that the California petroleum refining sector is undergoing significant consolidation. In 1985, the state supported more than 40 refinery operations. Over the next four decades, that number has fallen to under a dozen. Notably, during the same period, in-state refining capacity declined much more slowly, from 2.38 million barrels per day in the mid-1980s to roughly 1.64 million barrels per day now. As this history of California refineries shows, the industry has gradually consolidated its operations, closing smaller refineries and concentrating production at larger, more efficient facilities, in response to market conditions.

That slow but steady decrease in refining capacity mirrors downward demand for refined gasoline and makes business sense. Gasoline consumption in California peaked 20 years ago and has been declining ever since. Consumer desire for more efficient vehicles and state climate policies promoting zero and low emission vehicles are driving these consumption trends. The same factors will continue to shift consumer demand downward over the coming years, although current federal policy reversals could temporarily slow the rate of change.

Reading these tea leaves, two more California refineries have announced closures in the coming months – Valero in Benicia and Phillips 66 in Los Angeles – potentially reducing current statewide capacity by up to 17 percent. These companies are making long-term investment decisions based on future market projections. But refinery closures make the long-term decline in refining capacity lumpy – it comes in chunks – while the gasoline demand curve declines more smoothly over time. This is where the panic comes in: State officials worry that demand will temporarily exceed supply, driving up pump prices in the near term.

Oil industry trade associations and consultants are playing off these concerns with all manner of radical ideas, including rolling back most of California’s innovative climate policies, passing a new refinery investment tax credit, and even encouraging a federal take-over of California’s refineries. Perhaps recognizing the folly of such proposals, the industry seems to have settled on a legislative proposal that would exempt all new oil drilling from the California Environmental Quality Act (CEQA) – the state’s foundational community-right-to-know law – for the next decade.

This proposal is gaining traction because it sounds vaguely reasonable, but it actually makes no sense. The industry intimates that its own long-term business decisions to close refineries could be reversed if California just drilled more oil, and it suggests that such drilling is hampered by CEQA, which holds up drilling permit approvals. Every part of this claim is inaccurate.

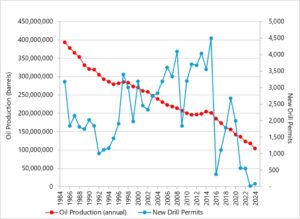

In-state crude oil production is a function of geology and economics, not environmental laws. Over the last four decades, crude oil production in California has fallen steadily and fairly sharply, starting long before state climate policies kicked in. Today’s production is a mere one-quarter of what it was in 1985. This continual decline has persisted regardless of the number of state drilling permits issued or the market price of crude oil.

What’s going on? California has been pumping oil and gas at furious rates for 150 years. Much of that early drilling was facilitated by the presence of natural gas deposits in oil reservoirs, which creates pressure that allows crude oil to flow readily to the surface, often resulting in uncontrolled “gushers.” But the days of gushers are long gone, leaving behind substantially depleted oil fields containing heavy crude oil, often tucked into folded geology, that is difficult to extract. Today’s drillers typically inject steam or hot water into the reservoir to lower the oil’s viscosity and increase its flow, a process often fueled by burning natural gas. Those enhancement techniques are energy-intensive and expensive.

As California oil extraction becomes less cost-competitive with drilling in other oil-rich areas, the industry has looked elsewhere for feedstock. The result: In-state production of crude continues to decline across California, including in historic Kern County oilfields, and refineries now import roughly 75 percent of the crude oil they process, mostly through our ports. That market development is not caused by a lack of drilling approvals. Indeed, nearly half of recently-approved drilling permits have gone unused.

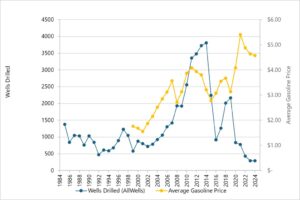

California’s WellSTAR database tells the story. Historically, rising gasoline prices have prompted new in-state drilling. But in recent years, the drilling of new wells in California has become uncoupled from gasoline prices, and already-approved drilling permits go unused as refiners choose to source crude feedstock from elsewhere in the global oil market. There is no evidence that approving more in-state wells will change these basic economic facts.

Indeed, with global oil prices projected to continue falling into next year, California crude is likely to become even less cost competitive. Although the state still ranks third domestically in terms of refining capacity (after Texas and Louisiana), facility operators understand the reality of both declining in-state crude oil production and declining California demand for gasoline. It is that reality that lies behind recent industry decisions to consolidate, convert, or close in-state refineries. It has little or nothing to do with CEQA or the speed at which the state issues new drilling permit approvals.

If CEQA is not the cause of oil refinery closures, its legislative evisceration cannot be the solution to lawmaker concerns about temporary impacts on pump prices. What, then, are real solutions that might smooth California’s inevitable transportation fuel transition? Energy experts have suggested many, including (1) enhance the ability of ports to increase imports; (2) reduce exports of California-refined gasoline to Nevada and Arizona; (3) reassess the need for California’s special blendstock requirements; and (4) subsidize refinery operations to keep the doors open while gasoline demand aligns with supply. Each of these options has pros and cons that require careful evaluation. But disenfranchising local communities by gutting CEQA is not the answer to anything.

Deborah A. Sivas is the Luke W. Cole Professor of Law at Stanford Law School and directs the Environmental and Natural Resources Law and Policy Program and the Environmental Law Clinic.

This post was also published on the Climate and Energy Policy Program blog.